The Construction Emissions Disclosure Gap: Why Scope 3 Category 1 Feels Impossible for GCC Builders

Scope 3 Category 1, the cradle-to-gate emissions of purchased goods and services such as concrete, steel, and aluminium, accounts for the large majority of a construction company’s carbon footprint and is the most difficult category to report. In the GCC, the gap is wider because the library of verified Environmental Product Declarations is limited and supply chains are heavily subcontracted. Regulation, procurement requirements, and the EU’s carbon border mechanism are now making disclosure unavoidable. Contractors can close the gap in stages using the GHG Protocol methods hierarchy rather than waiting for complete data.

Key takeaways:

- Category 1 (purchased goods and services) dominates a builder’s footprint, led by concrete and steel; direct diesel and electricity are minor by comparison.

- The principal GCC barrier is a limited library of local Environmental Product Declarations (EPDs), which forces reliance on non-representative foreign emission factors.

- The UAE mandates Scope 1 and 2 reporting, with a first full-compliance deadline of 30 May 2026 and Scope 3 anticipated from 2027.

- Tender requirements (including NEOM and public projects) and the EU Carbon Border Adjustment Mechanism add commercial and export pressure alongside regulation.

- The GHG Protocol allows a staged approach: spend-based screening, then activity data, then supplier-specific EPDs. A defensible baseline is achievable within weeks.

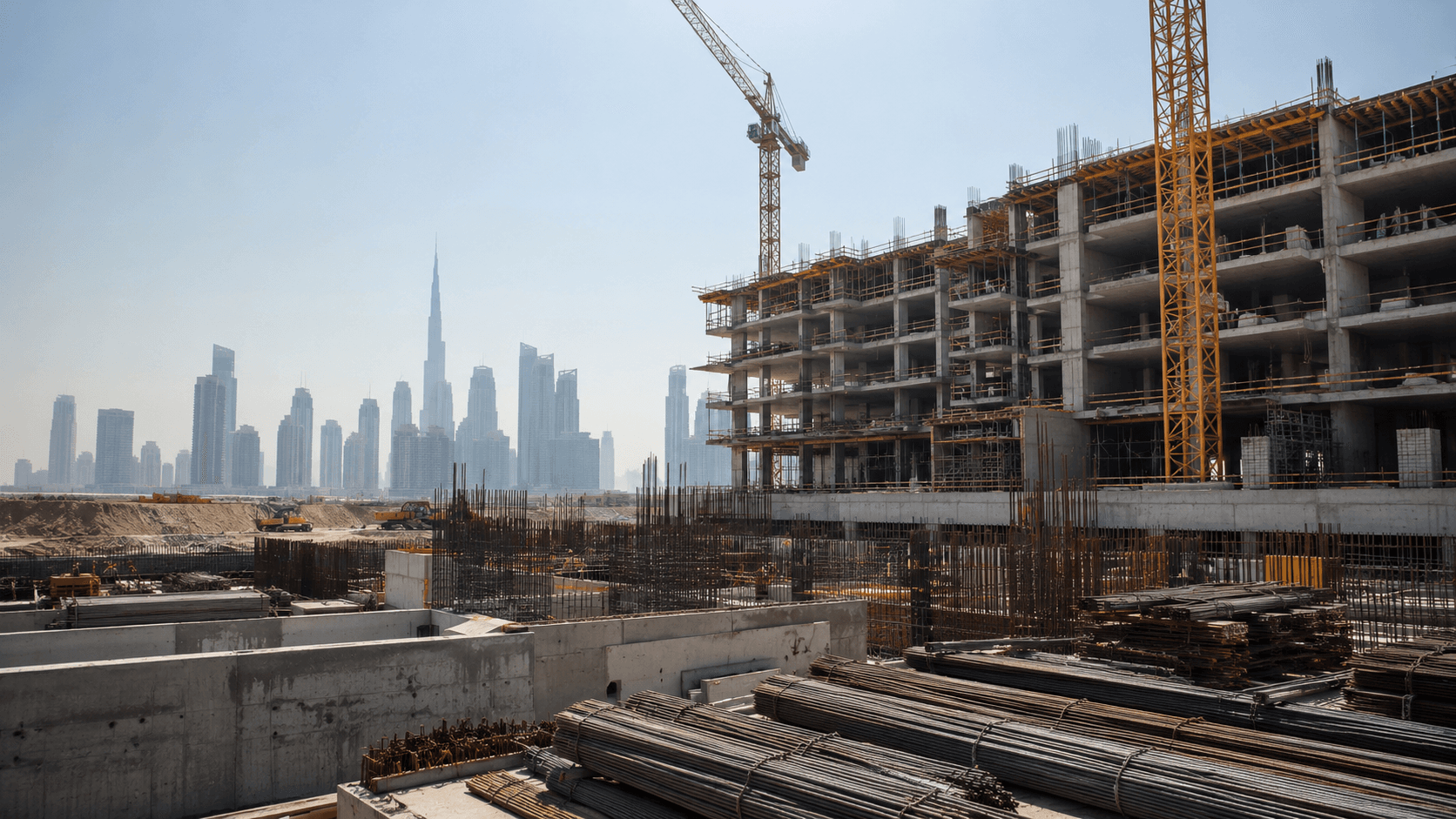

Most GCC contractors can account precisely for the diesel their equipment consumes, yet struggle to quantify the emissions embodied in the concrete and steel they purchase. That gap falls under Scope 3 Category 1, purchased goods and services, which represents the large majority of a construction company’s carbon footprint and is the category the industry is least equipped to report.

This article examines why the gap is particularly pronounced in the GCC, why the challenge is a function of current data practices rather than an inherent limitation, and what contractors can do before regulators and project owners cease to accept estimates.

Scope 3 Category 1 in a construction context

Scope 3 Category 1 covers the upstream, cradle-to-gate emissions of all purchased goods and services. For a contractor, this includes concrete, steel, aluminium, glass, insulation, mechanical, electrical, and plumbing (MEP) equipment, and subcontracted services. Under the Greenhouse Gas Protocol (GHG Protocol) technical guidance, a construction company should collect activity data, such as tonnes of steel and cubic metres of concrete, and apply supplier-specific emission factors wherever possible.

In the built environment, these emissions are more commonly described as embodied carbon. The two frameworks measure the same activity: lifecycle stages A1 to A3 in a whole-life carbon assessment correspond to Category 1 in a corporate inventory. One accounting distinction is worth noting. A developer that capitalises a building may report these emissions under Category 2, capital goods, whereas a contractor purchasing materials for a client’s project reports them under Category 1. The underlying data challenge is the same in both cases.

For teams still establishing the fundamentals, Coral’s explainer on operational vs. value chain emissions provides a useful starting point.

Why purchased materials dominate the construction footprint

Buildings are composed of two of the most carbon-intensive commodities in industrial production. Cement alone accounts for roughly 7 to 8 percent of global CO2 emissions, and the buildings and construction sector as a whole for around 37 percent of global CO2 emissions once materials are included. A contractor’s direct diesel and electricity consumption is minor by comparison with the steel frame and concrete core.

These dynamics are amplified in the GCC. The regional construction market is worth around USD 350 billion in 2026, Saudi Arabia represents the largest single market at approximately 40 percent, and the region favours hot-climate, high-rise, concrete-intensive development. Higher concrete use per square metre translates into greater Category 1 emissions per unit of revenue than in almost any other sector.

The barriers to reporting Category 1 in the GCC

Four factors explain the difficulty, none of which reflects a lack of intent.

1. Limited availability of EPDs: Supplier-specific reporting depends on Environmental Product Declarations, the verified carbon labels for building products. Europe maintains tens of thousands; the GCC’s library remains thin and uneven. Published analysis of concrete EPDs shows Saudi manufacturer-specific declarations recording some of the highest impacts globally, and for many regional products no declaration exists. Producing one takes 10 to 16 weeks per product, so supply expands more slowly than the project pipeline.

2. Reliance on non-representative emission factors: Where local EPDs are unavailable, contractors default to European or North American database factors. These assume different grid intensities, cement chemistry, and transport distances. An inventory built on this basis may misstate emissions in either direction and is difficult to defend under audit. Coral’s analysis of when local sourcing backfires for Scope 3 illustrates how significantly geography can alter the result.

3. Fragmented, subcontracted supply chains: A main contractor on a GCC mega-project may sit above hundreds of subcontractors and thousands of material deliveries. Under the GHG Protocol, a subcontractor that purchases its own fuel and supplies its own equipment falls within the main contractor’s Category 1 as a purchased service. Collecting primary data across that chain manually does not scale. This reflects the same dynamic described in the trickle-down effect of corporate climate action, compounded here by longer chains and multiple currencies.

4. Misalignment between project and reporting cycles: A tower may take four years to construct, while corporate GHG inventories are prepared annually. Determining which reporting year should absorb the embodied carbon of a partially completed structure is a recognised methodological issue that UKGBC has identified as a structural mismatch between building emissions and Scope 3 reporting cycles.

Regulatory and market pressure is intensifying

While the data infrastructure is still developing, the requirements are already in place.

Regulation. The UAE’s Federal Decree-Law No. 11 of 2024 entered into force on 30 May 2025 and established its first full-compliance deadline on 30 May 2026, with fines ranging from AED 50,000 to AED 2 million for entities that fail to measure and report. Scope 1 and 2 reporting is mandatory, and Scope 3 reporting is anticipated to become mandatory from 2027. Contractors that defer preparation until Category 1 is named explicitly will face a compressed implementation timeline.

Procurement. No GCC country has yet legislated a carbon cap on buildings, but tender requirements are increasingly filling that role. NEOM requires product-specific EPDs for all structural materials, and the UAE Ministry of Energy and Infrastructure targets a minimum 5 percent embodied carbon reduction on public projects. Estidama, Mostadam, and GSAS, the region’s green building rating systems, all reward EPD-backed materials. Suppliers without verified data are increasingly excluded at the shortlist stage.

Export exposure. The EU’s Carbon Border Adjustment Mechanism (CBAM) entered its definitive phase in 2026, and GCC steel and cement exporters to Europe now carry a price on their embedded emissions. The same producers supply domestic projects, so the verified data generated for CBAM will progressively feed regional EPDs, a constructive by-product of the mechanism.

Finance. Lenders and insurers are already repricing carbon-exposed buildings, as discussed in Coral’s analysis of stranded assets in GCC real estate. Embodied carbon disclosure is becoming a factor in how capital assesses project risk.

A staged approach to closing the gap

Complete, immediate, and manual accuracy is not achievable. Credible, staged reporting is. The GHG Protocol permits a hierarchy of methods, which contractors can apply progressively.

Step 1: Screen using spend data. Map procurement ledgers to spend-based factors to identify emissions hotspots. In construction, these are almost always concrete and steel, followed by aluminium and MEP. This exercise takes weeks rather than years and indicates where primary data collection is most valuable.

Step 2: Convert hotspots to activity data. Bills of quantities, delivery notes, and Building Information Modelling (BIM) models already contain quantities in tonnes and cubic metres. Combining these with regional or product-specific factors improves accuracy where it has the greatest effect.

Step 3: Require EPDs where volume justifies it. A contractor procuring hundreds of thousands of cubic metres of concrete has sufficient purchasing power to make EPDs a supplier prequalification requirement. GCC producers are responding: blended cements incorporating slag and fly ash are already available and can reduce concrete emissions by 25 to 35 percent, supported by verifiable data.

Step 4: Automate the reporting pipeline. Invoice-level ingestion, factor mapping, and audit trails are better suited to software than to manual processes. This is the transition described in Coral’s analysis of AI carbon management in the GCC: from periodic reporting exercises to continuous carbon data infrastructure. Because these figures will be reviewed by auditors, verifiers, and regulators, the systems producing them must be reliable throughout. Coral’s discussion of the trust stack explains why this is particularly important in ESG software.

The disclosure gap is a data supply chain challenge rather than a fundamental constraint. Contractors that address it on that basis in 2026 will be better positioned to compete for tenders in the years that follow.

FAQ

Is embodied carbon the same as Scope 3 Category 1?

Largely, yes. Cradle-to-gate embodied carbon (stages A1 to A3) of purchased materials sits within Category 1 for a contractor. Developers that capitalize buildings may report it under Category 2, capital goods.

Do GCC contractors legally have to report Scope 3 today?

Not currently. The UAE climate law mandates Scope 1 and 2 reporting, with Scope 3 anticipated from 2027. In practice, tender requirements and client supply-chain requests are the binding force.

What if my suppliers have no EPDs?

Apply the GHG Protocol hierarchy: spend-based screening first, then activity data with regional factors, then supplier-specific data for the highest-volume materials. Document the method and refine it year on year.

Where should a contractor start?

With existing procurement data. A spend-based screen of the prior year’s ledger identifies the emissions hotspots and provides a defensible baseline within weeks.

How Coral closes the Category 1 gap

Coral’s Emissions Management System ingests procurement data, maps it to the appropriate emission factors, and produces audit-ready Scope 1 to 3 inventories aligned with the GHG Protocol and ISO 14064. Book a demo to see how GCC contractors can convert a disclosure gap into a competitive advantage in tendering.

متعلقہ مضامین

Waste-to-Energy in Gulf Cities: Climate Solution or Incineration Greenwashing?